Let’s stop pretending that savings money is just a matter of “willpower” or skipping a few avocado toasts. If we are being completely real, the modern economy is basically a giant, hyper-optimized machine designed to separate you from your paycheck before you even realize it’s gone.

Between auto-renewing apps you forgot you signed up for, targeted ads that read your mind, and a cost of living that feels like a cruel joke, keeping money in your bank account is an actual psychological battle.

Here is the completely raw, unvarnished truth about how to protect your cash without making your daily life feel miserable.

The Anti-Budget Manifesto: How to Keep Your Cash in a World Designed to Drain It

We’ve all experienced the quiet panic of checking our banking app on a random Tuesday, staring at a double-digit balance, and trying to trace back exactly where the money went. You didn’t buy a ticket to space. You didn’t go wild at a luxury boutique. You just… lived. A couple of food deliveries here, a subscription renewal there, an unexpected gas station run, and suddenly your hard work has evaporated.

The biggest lie we’ve been fed about personal finance is that saving requires suffering.

We’re told to track every single cent on a spreadsheet, feel guilty about a $5 coffee, and stop going out with friends. That isn’t a sustainable financial strategy; it’s a recipe for burnout. The moment a budget feels like a prison sentence, you’re going to break out of it and go on a revenge-spending spree.

True financial freedom isn’t about restriction. It’s about building an automated defense system that protects your future self from your current impulses. It’s shifting from a mindset of “I can’t afford this” to “I am actively choosing what deserves my energy.”

The Financial Cheat Code: Pay Yourself First

Most people handle their paycheck with a fatal flaw: they pay everyone else first. They pay the landlord, the electric company, the streaming services, the grocery store, and then they tell themselves they will save whatever is left over at the end of the month.

But guess what? The universe abhors a financial vacuum. If there is money sitting in your checking account, a random expense or a sudden impulse will rise up to claim it.

The only way to win this game is to take your cut before anyone else touches a dime. Set up an automatic transfer that triggers the exact same day your direct deposit hits. Move a realistic slice of your check—even if it’s just $25 or 10%—directly into an account you don’t easily see. By making savings the default setting rather than an afterthought, you force your lifestyle to adapt to the remainder. If you don’t see it, you won’t spend it.

Burn the Budget, Build a Spending Plan

Traditional budgeting feels like a strict diet—it’s entirely focused on what you’re forbidden to do. A spending plan, on the other hand, is a blueprint for your priorities. It gives you explicit permission to spend money on things that actually bring joy to your life by ruthlessly cutting out the things that don’t.

When you stop viewing money as a math problem and start viewing it as traded life energy, things click. If you value traveling or eating at incredible restaurants, put it in the plan. Own it. Spend that money without an ounce of guilt. But to fund that joy, you have to be totally honest about the leaks—the gym membership you haven’t used since January, or the premium app tiers you don’t actually need.

The 24-Hour Digital Cool-Down

Online shopping apps are designed by world-class data scientists to put you in an emotional, impulsive state. The “One-Click Buy” button is a psychological trap. It removes the natural friction of spending, turning a financial decision into a mindless hit of dopamine.

The easiest way to fight back is to install a mandatory speed bump: the 24-hour rule.

When you find something online that you suddenly feel will change your life, add it to your cart, and then completely close the app. Walk away for a full day. In those 24 hours, the emotional fog clears, the dopamine spike levels out, and your logical brain steps back into the room. More than half the time, you’ll look at that open tab the next day and realize you don’t even want the item—you were just bored, tired, or stressed.

Dodging the “Upgrade” Trap (Lifestyle Inflation)

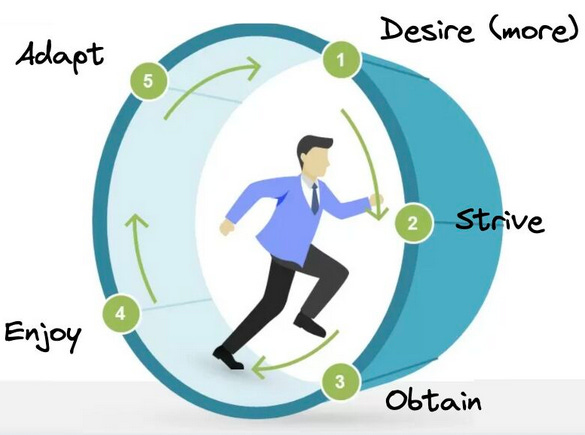

It’s a bizarre human phenomenon: you finally get that hard-earned raise or promotion, but somehow, your bank account feels exactly as empty as it did before. This is the silent killer known as lifestyle inflation.

The moment we start making more money, our definitions of “normal” instantly shift.

- A little extra cash means we stop cooking and start ordering premium delivery.

- A bonus check turns into a justification for a higher car payment.

- A salary bump convinces us we need a bigger apartment.

There is nothing wrong with leveling up your life, but if your lifestyle matches your income dollar-for-dollar, you are running on a golden hamster wheel. You’re making more, but you aren’t any more secure. The move here is simple: whenever your income goes up, immediately direct at least half of that new money into your automated savings or investments before you ever get a chance to taste it. Upgrade your life with the rest, but let your safety net grow faster than your bills.

Needs vs. Wants: The Brutally Honest Filter

There is absolutely zero shame in spending money on your wants—that is the whole point of earning a living. The danger only arises when you blur the line and start treating conveniences as non-negotiable entitlements.

We like to intellectualize our desires. We tell ourselves that a new laptop, a specific wardrobe upgrade, or a high-end grocery delivery service is a “need” because it helps our productivity or health. But let’s call a spade a spade.

| Category | The Textbook Definition | The Realist Version |

| The Need | Food, shelter, basic utility, healthcare. | Things that keep you alive, housed, and employed. |

| The Want | Upgrades, convenience, aesthetics, status. | Things that make the baseline version of life more comfortable or stylish. |

Tuning Out the Social Media Mirage

We are the first generation in human history to spend hours every day looking at a highly polished, heavily filtered highlight reel of the richest people on earth. We scroll through Instagram or TikTok and see peers on luxury yachts, driving flawless cars, and unboxing expensive gear.

It creates a deep, subconscious pressure to spend money just to look like we belong.

But you have to realize that appearances are the cheapest thing money can buy. A massive credit card limit can make anyone look rich for a few months. A steep car loan can put anyone in a luxury vehicle. What you don’t see behind those flawless photos is the crushing debt, the late-night anxiety, and the complete lack of financial breathing room. True wealth is silent. It’s the money you don’t spend. It’s the freedom to walk away from a toxic job or handle an emergency without panic.

The Failsafe: The Anti-Panic Fund

Life does not care about your plans. Your car’s alternator will die, your phone screen will shatter, or a medical bill will land in your mailbox at the absolute worst possible moment. Without a cash cushion, these minor life hiccups turn into full-blown financial catastrophes that force you onto high-interest credit cards.

An emergency fund isn’t an investment strategy; it’s an insurance policy for your sanity.

“An emergency fund transforms a life-altering crisis into a temporary financial inconvenience.”

If the idea of saving six months of living expenses feels completely impossible, stop looking at the mountain. Focus on saving just $500. Then $1,000. Having even a grand tucked away in a dedicated “do not touch” account completely changes the energy of your life. You stop living on the defensive, waiting for the other shoe to drop, because you know you have the cash to handle the hit.

Give Yourself Radical Grace

You are going to mess up. You are going to have a brutal week at work, break your rules, and spend too much money on an expensive night out or an absurd online purchase.

When that happens, please do not trash your entire system and declare yourself a failure. You aren’t bad with money; you’re just a human being navigating an incredibly expensive world.

Financial health isn’t built on a single perfect month; it’s built on hundreds of tiny, invisible choices over the course of years. If you overspend on Friday, don’t throw away the whole weekend. Reset on Saturday morning. Check your accounts without judgment, trust your automated systems, and remember that every time you choose to save a dollar, you are buying a piece of your own future freedom.

FAQs

1. What is the best way to start saving money?

Start by setting aside a small amount from every paycheck and automating your savings.

2. How can I avoid impulse spending?

Use the 24-hour rule and wait before making non-essential purchases.

3. Why is an emergency fund important?

It helps cover unexpected expenses without creating debt.

4. How do small savings habits make a difference?

Small, consistent savings add up significantly over time through compounding.

5. What is lifestyle inflation?

Lifestyle inflation happens when your spending increases as your income grows, making it harder to save.